New Hampshire Trusts

We combine the favorable trust and tax laws of New Hampshire with 140 years of wealth management experience.

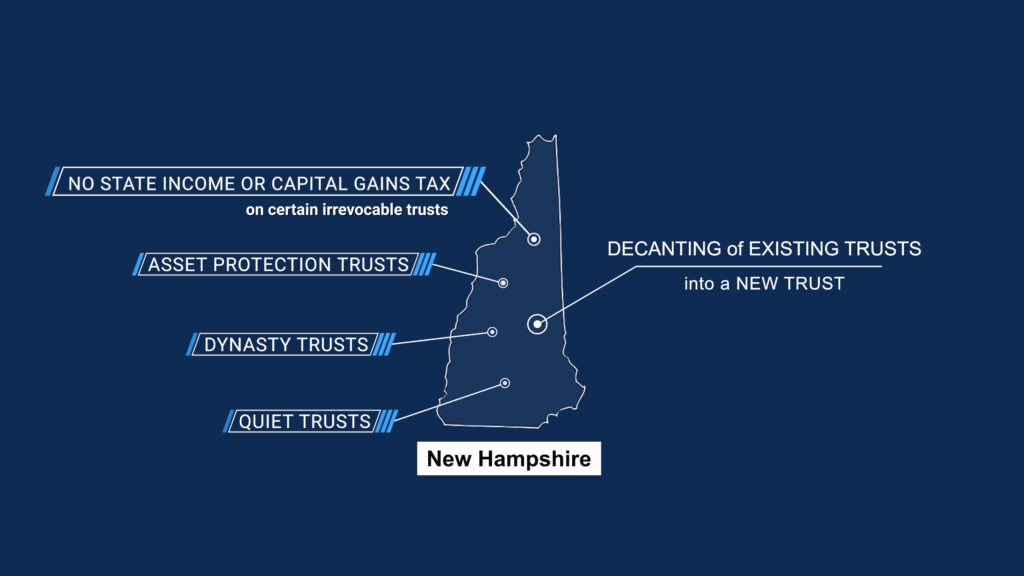

New Hampshire's Trust Advantages

The Granite State's trust laws are available to families nationwide and internationally. Their use can deliver tremendous benefits in tax savings, asset protection, and multi-generational asset transfer as well as several other advantages.

Meet Your Team

Discover Our Insights

Asset Protection Trust Benefits

New Hampshire has become one of the most progressive states amongst the group to permit the Domestic Asset Protection Trust ("DAPT") and, as a result, an attractive jurisdiction to utilize.

Adaptable Trusts: Changing the Game Plan at Halftime

Building adaptability into trusts can provide flexibility to adjust to unforeseen changes in laws and other factors. Trust "decanting" is an option in some cases.

Sustainable Investing and Trusts

Learn about New Hampshire laws which make it one of the few states to provide trustees more flexibility to pursue sustainable investing strategies.